New Economics Foundation Explain How the UK Benefits System Was Hollowed Out Over 10 Years

Sunday 28 February, 2021 Written by New Economics Foundation, Sarah ARNOLD, Dominic CADDICK, Lukasz KREBEL

NEW ECONOMICS FOUNDATION - If we’d stuck with the social security we had a decade ago, 1.5 million fewer people would be living in poverty...

Our social security system looks very different to how it did 10 years ago. While a few changes have been for the better, overall our social safety net has got significantly weaker in terms of level of support provided. Cuts have reduced the ability of the system to support incomes during the current economic downturn, by taking £14bn out of the welfare system since 2010/11, falling to £7bn if the uplift is maintained.

Our new analysis has found that, come April, the poorest 20% of households, both in or out of work, will be £750 a year (6%) worse off than they would have been back in 2010. We’ve found that if the system inherited by the coalition government had been maintained, 1.5 million fewer people would be in poverty. Maintaining the £20 uplift in universal credit and tax credits would go some way to reversing the reduction in payments to households over the past 10 years — but even with the uplift, the poorest households will still be on average £260 a year (2%) worse off than they would have been under the 2010 system, whether in or out of paid work.

As millions have become unemployed over the last year, and millions more are furloughed on reduced pay, our social security system should be playing an important role in supporting incomes throughout the crisis. The most recent data (for September to November 2020) shows an estimated 1.7 million people are officially unemployed, with 4.1 million “temporarily away from work”. Of the latter, over a quarter of a million were away from work because of the pandemic and receiving no pay. Many people have been excluded from the furlough and self-employment support schemes: for example the Resolution Foundation found that 500,000 self-employed people were without work and not receiving support last September. And these figures are set to worsen, with unemployment expected to reach 2.6 million in the middle of 2021.

And while the furlough scheme has protected many incomes through the crisis, in 2020 52% of furloughed people ended up on less than minimum wage. This is because furlough only protects 80% of income, and those on lower wages are more likely to be furloughed, according to the Office for National Statistics (ONS).

The social security system has picked up the slack, with the number of people on universal credit more than doubling from 2.7 million in December 2019 to 5.9 million in December 2020. Many of these claimants are using the system to supplement low incomes, with 40% of universal credit claimants in work.

“… our social security system should be playing an important role in supporting incomes throughout the crisis”

Social security spending overall has grown throughout the pandemic as unemployment has risen, just as it has through prior recessions. It is natural that spending has risen during the downturn, in order to protect and stabilise incomes. But although the number of people relying on welfare has risen during the pandemic, the level of support per person is still significantly lower than it was at the start of the decade (even with the government’s temporary £20 uplift to universal credit and working tax credit).

This is due to a range of government decisions about social security aimed at reducing its overall cost over the last 10 years. These include freezes to the payment levels, a cap on the maximum benefits a household can receive, a limit on the number of children a family can claim support for, limits to the local housing allowance, and means testing of child benefit. And there has been a significant shift towards conditionality for claimants, with increasing use of sanctions if conditions are not met. The sanctions regime has been criticised as one of the most punitive in the world.

These decisions have impacted the lowest-income households most of all. Our new analysis has found that if the 2010/11 benefits system had been maintained in real terms, instead of being made more punitive, people would be on average much better off and the system would be much more effective in supporting incomes and stabilising the economy. This is true even if the £20 uplift to universal credit and working tax credits is maintained, although the uplift does mitigate some of the cuts. We drew inspiration from similar previous analysis by the Resolution Foundation in 2019 and the Joseph Rowntree Foundation (JRF) in 2020 (for full details of our analysis, see the methodology notes at the end). This analysis is not meant to illustrate a desire to return to our old system, simply to set the current system in context.

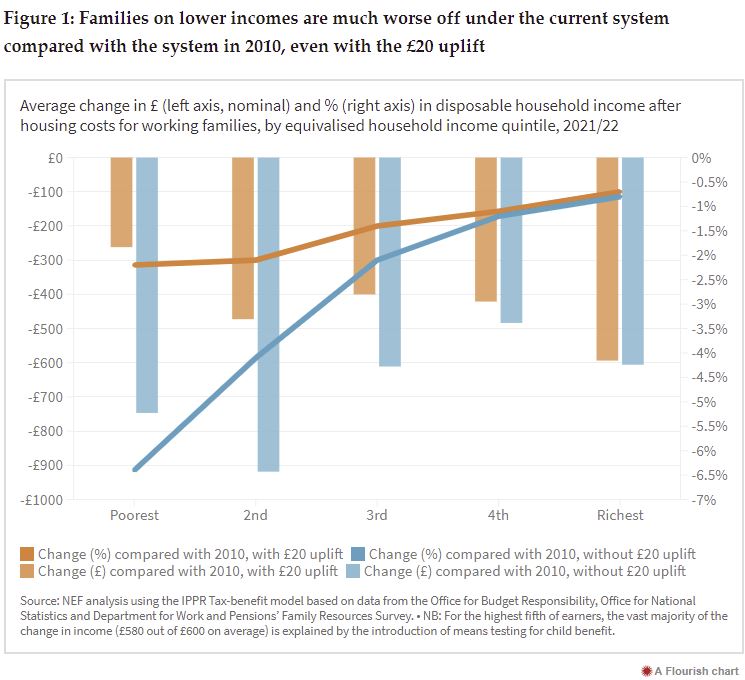

Our results show that on average, people across the income distribution are worse off as a result of changes to the social security system over the last decade. These figures are particularly striking because they do not just show those who receive any particular benefit: on average all income quintiles of the population are worse off (see Figure 1 below). The lowest fifth of earners are on average 6% worse off, or receiving £750 less a year, compared to the 2010/11 system — and are still worse off even if the £20 uplift is maintained. Higher earners are worse off compared to where they would have been mainly due to the introduction of child benefit means testing for high earners. For the highest fifth of earners, £580 of the £600 shortfall compared with the 2010 system is explained by the introduction of means testing for child benefit. Overall, we found that if the 2010/11 benefits system had been maintained, there would be 540,000 fewer households in absolute poverty, including 830,000 adults and 700,000 children, compared to the expected benefits system next year.

Figure 1: Families on lower incomes are much worse off under the current system compared with the system in 2010, even with the £20 uplift

The impacts also vary significantly by family type and work status. On average, out-of-work families have lost £1,160 in annual income due to changes to the benefit system since 2010 (see Table 1). This figure reduces to £440 if the £20 uplift stays in place. Working families have also lost out, with a £460 reduction compared to if the 2010 benefits system was in place. Similarly, this reduces to £240 if the £20 uplift remains.

Many families are currently struggling, but for different reasons. In general, those with children are now much worse off than they would have been under the 2010/11 system. But those without children did not, on average, have access to the necessary incomes needed to live at a socially acceptable standard even at the start of the decade — and still don’t now.

Single parents in particular are much worse off, losing an average of £2,700 a year if they are not in work, and an average of £1,100 a year if they are. For couples with children the respective figures are £2,450 and £1,250.

Table 1: Single parents and couples with children lose out the most, on average, compared to the 2010/11 benefit system, with and without the £20 uplift

Change in annual disposable income in cash and % comparing the 2010/11 system to the UK’s current safety net and a continuation of the £20 per week uplift (respectively), by family type containing those of working age in 2021/22

Without £20 uplift

|

At least one household member working |

Not working |

|||

|

Annual income loss |

% income loss |

Annual income loss |

% income loss |

|

|

Couple with children |

£1,250 |

2% |

£2,450 |

9% |

|

Couple without children |

-£70 |

-0% |

£1,280 |

8% |

|

Single with children |

£1,100 |

3% |

£2,700 |

12% |

|

Single without children |

-£50 |

-0% |

£650 |

10% |

|

All families |

£460 |

1% |

£1,160 |

10% |

With £20 uplift

|

At least one household member working |

Not working |

|||

|

Annual income loss |

% income loss |

Annual income loss |

% income loss |

|

|

Couple with children |

£890 |

1% |

£1,930 |

7% |

|

Couple without children |

-£145 |

-0% |

£810 |

5% |

|

Single with children |

£360 |

1% |

£2,300 |

10% |

|

Single without children |

-£180 |

-1% |

£210 |

3% |

|

All families |

£240 |

1% |

£440 |

4% |

Source: NEF calculations using the Family Resources Survey and the IPPR tax benefit model

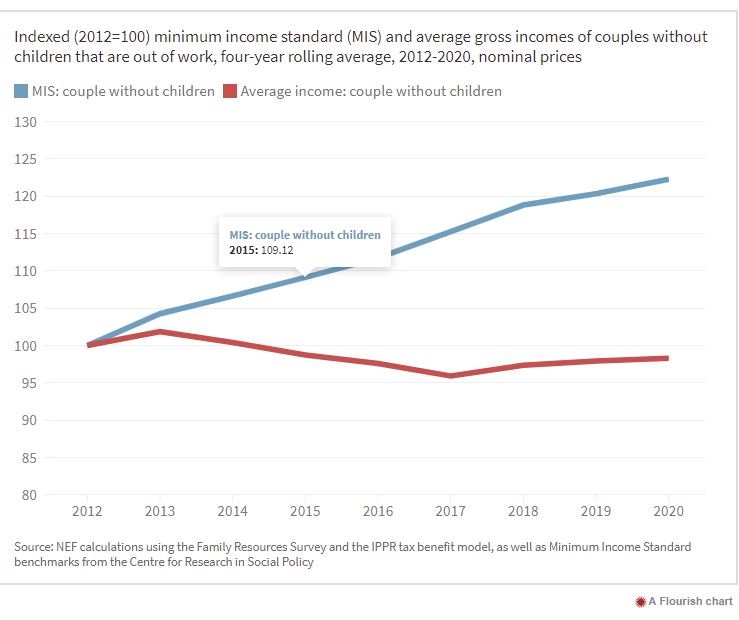

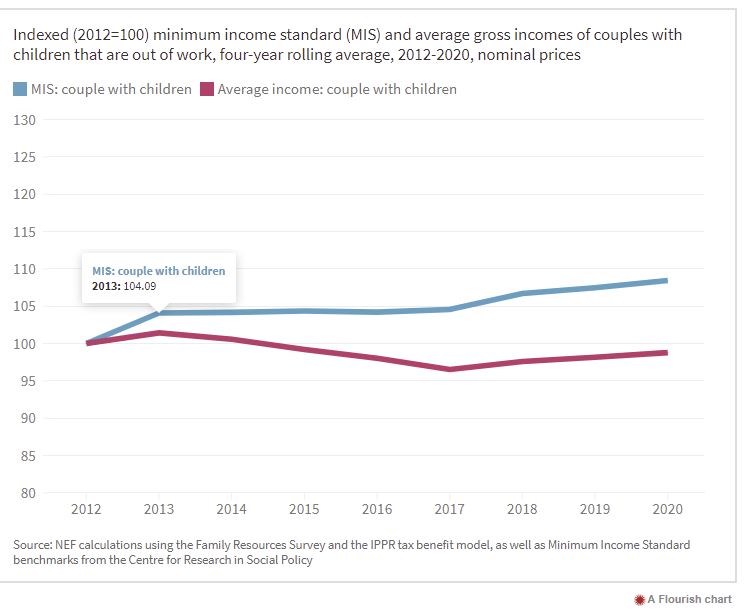

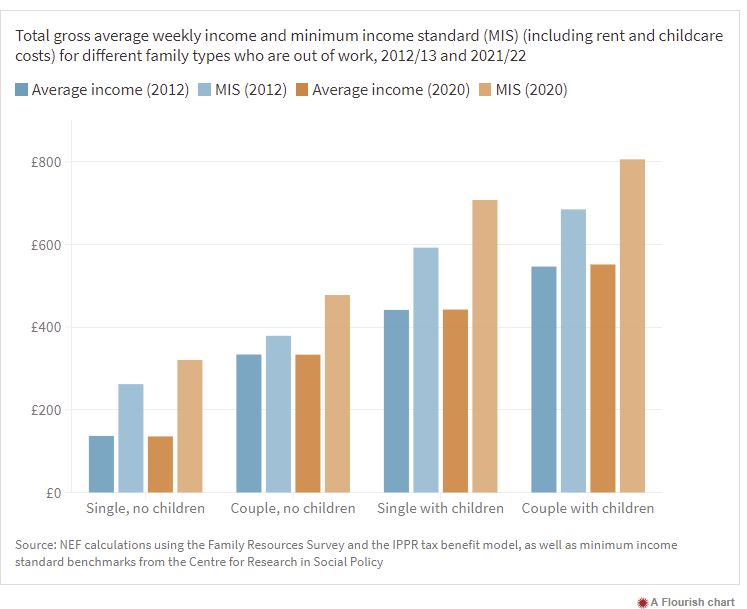

And while the level of social security support has fallen, the cost of living has been rising over the last decade. In fact, the gap between average incomes for out-of-work families compared to the minimum income standard — a measure of what is needed to live a socially acceptable quality of life in the UK — has been widening. As illustrated by Figure 2, this is the case regardless of whether people have children or not, are single or are in a couple — though the effect is most pronounced for people without children.

Figure 2: The gap between cost of living and income required for a socially acceptable standard has widened over the last decade for out of work families containing working-age people compared to incomes

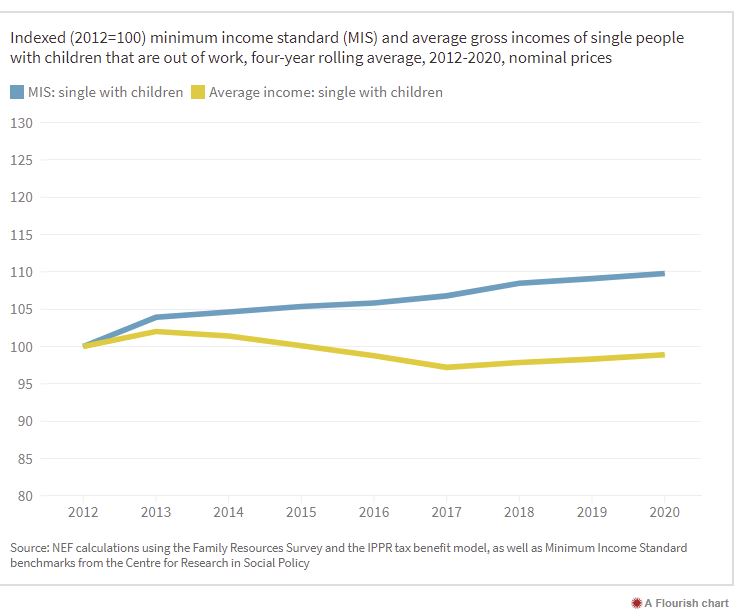

As Figure 3 shows, for single people without children, this has been a particular struggle. For them, income as a proportion of socially acceptable living standards was low at the start of the decade (52% in 2012) — and on average this has dropped to just 42% by 2020, even with the £20 uplift. (Note that this figure is for gross income and therefore underestimates the gap.).

Figure 3: The cost of living has been rising while the incomes of people out of work have more or less remained frozen over the last decade

Having a weaker system of welfare provision is concerning for two reasons. Firstly, many families are struggling to put food on the table. This was true prior to the pandemic, with the Trussell Trust reporting foodbank usage increasing across their networks by 73% between 2015/16 and 2019/20, but usage has further increased during the pandemic: in April 2020 there was an 89% increase in number of emergency food parcels given out than the previous year.

And secondly, we are in a sharp downturn, with an annual GDP fall of 9.9% in 2020 — the largest yearly fall on record. During downturns, social security has a vital role in boosting spending by targeting payments towards those at the bottom end of the income distribution. The government itself recognised that these historical cuts limit the ability of the social security system to provide a stabilisation role during the economic crisis, and responded with £20 temporary uplifts to the universal credit and working tax credit main elements. But this is far from enough, and is due to be removed at the end of March. Changes to working age benefits modelled have taken £14 billion out of the welfare system since 2010/11, falling to £7 billion if the uplift is maintained.

Successive government policy decisions over the last decade have significantly hollowed out the social security system. At the very least the government should maintain the £20 uplift and extend it to legacy benefits. But it is increasingly clear that this will not be enough on its own to protect incomes or stabilise the economy. Although we are not at all suggesting the government returns to the 2010 system, which was a fragmented and confusing system, it must go further to ensure the UK’s safety net is fit for purpose, both now, and for the future.

People in the UK need a living income, to make sure all of us can have a decent standard of living. A living income should have a minimum income guarantee at its heart, making sure that everyone has enough money to live a decent life. With a minimum income guarantee, everyone who needs it would receive at least £227 a week throughout the rest of the pandemic – making the UK economy stronger, bringing money back into local communities and making sure everyone has enough to thrive, not just survive.

Notes

The analysis looks at the effects of the current benefits system on household incomes compared to 2010. It does this by comparing outcomes under the current 2021/22 benefits system to a situation where all universal credit claimants are instead on the legacy benefits that universal credit is replacing, namely: housing benefit, income support, jobseeker’s allowance (JSA), employment and support allowance (ESA), working tax credit (WTC) and child tax credit. Furthermore, child benefit is also restored to how it operated in 2010. On top of this, policy decisions related to these benefits in the 2010 – 2020 period are reversed. This includes: changes to child tax credit eligibility, removing the benefits cap, removing the bedroom tax, reversing benefit freezes, removing means tested child benefit, keeping the work-related activity component of the employment and support allowance (ESA) and removing the time limit, removing the two-child limit from child tax credits and keeping the family element. Benefits freezes were reversed by adjusting 2010 level payments by consumer price index (CPI) inflation due to the government move to CPI over retail price index (RPI) for uprating in 2010. Results were obtained using the Institute for Public Policy Research (IPPR) tax-benefit model. Caps on local housing allowance could not be changed due to limitations of the model.

Comparisons to the £20 uplift take into account the £20 uplift to universal credit and £20 uplift to WTC, and do not include legacy benefits.

Results are shown in 2021/22 prices, by benefit unit.

Poverty figures reported are absolute poverty figures, showing the proportion of households with disposable income below 60% of the 2010/11 median wage, after household costs.

Figure 2 uses a four-year rolling average of the minimum income standard (MIS) and average income for different family types. The rolling average is used to account for methodological changes in how the MIS is calculated, with the composition of goods updated on a four-yearly basis. To match this approach, a four-year average is used for average incomes as well, which to some extent masks the £20 universal credit uplift but provides a fairer long-term comparison. MIS figures for those with children are specifically for two children (one aged 2 – 4; one primary school age) whereas average income figures with children include any family size.

![]()

ABC Note: The New Economics Foundation (NEF) is a British think-tank that promotes "social, economic and environmental justice". The foundation has 50 staff in London and is active at a range of different levels. Its programmes include work on well-being, its own kinds of measurement and evaluation, sustainable local regeneration, its own forms of finance and business models, sustainable public services, and the economics of climate change.

ABC Comment, have your say below:

Leave a comment

Make sure you enter all the required information, indicated by an asterisk (*). HTML code is not allowed.

Join

FREE

Here